Complete Guide to Income Tax Planning and Filing in India (2026)

Every year, millions of Indians face the same problem. March is ending, and they are scrambling to find investment proofs, calling their CA at midnight, and rushing to file their returns at the last moment. The stress is real. The mistakes are costly. And the tax savings? Mostly missed.The truth is,income tax planning and filing in India is not a one-week job. It is a 12-month process. And when done right, it saves you thousands - sometimes lakhs - in taxes every year.

This complete guide covers everything you need to know about income tax planning and filing in India for 2026. Whether you are a salaried employee, a business owner, or a freelancer in Bhopal or anywhere across India, this guide is for you.

What Is Income Tax Planning - And Why Does It Matter?

Income tax planning means arranging your finances in a way that reduces your tax burden legally. It is not about hiding income. It is about using the rules that the government has already written for your benefit.

Think of it this way. The government gives you multiple ways to reduce your taxable income - through investments, insurance, home loans, donations, and more. Tax planning is simply about knowing these options and using them smartly before the financial year ends.

So, why does it matter?

First, without a proper tax planning service, most people end up paying more tax than they legally need to. Second, they make rushed investment decisions in March just to save tax, instead of choosing options that also build long-term wealth. Third, poor planning leads to penalties, missed deadlines, and notice from the Income Tax Department.

A well-structured income tax planning and filing in India process helps you stay compliant, save money, and sleep better at night. That is the goal.

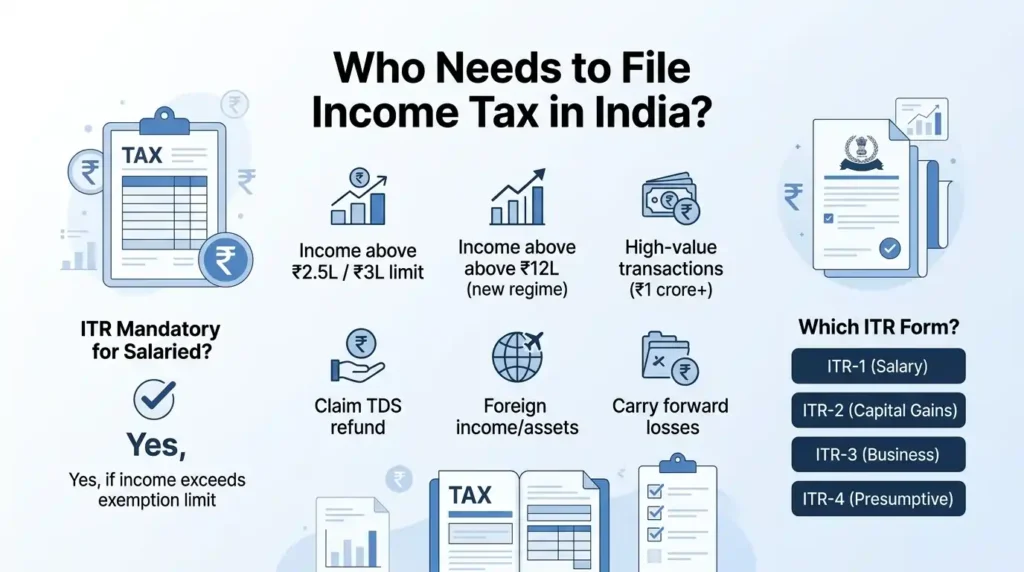

Who Needs to File Income Tax in India?

This is one of the most common questions people ask. The short answer is - more people than you think.

You must file an income tax filing service return in India if:

- Your total income exceeds the basic exemption limit (₹2.5 lakh under the old regime or ₹3 lakh under the new regime for individuals below 60 years)

- Your income is above ₹12 lakh under the new regime after applicable rebate

- You have made high-value transactions during the year, such as depositing over ₹1 crore in a savings account

- You want to claim a refund on excess TDS deducted from your salary or bank interest

- You have foreign assets or income from outside India

- You want to carry forward losses to future years

Even if your income is below the taxable limit, filing a return is still a good habit. It builds your financial credibility, helps with visa applications, and makes loan processing faster.

Is Income Tax Filing Mandatory for Salaried Employees?

Yes. If your gross salary exceeds the basic exemption limit, filing an income tax filing service return is mandatory. Even if your employer has already deducted TDS from your salary, you still need to file your ITR independently. Your Form 16 is not a substitute for filing.

Additionally, from April 2026, the new Income Tax Act 2025 has replaced the Income Tax Act 1961. The new law brings simpler language and cleaner processes - but the filing obligation remains unchanged.

Also Read - Top 10 Financial KPIs Every Startup CEO Must Track in 2026

Did You Know? Under the new tax framework effective from April 2026, a single "Tax Year" concept has replaced the confusing "Previous Year" and "Assessment Year" terminology. Now, income earned in Tax Year 2026-27 is filed within the same year. This makes tax planning timelines much easier to track.

Which ITR Form Should You Use?

Choosing the wrong ITR form is one of the most common mistakes taxpayers make. Here is a simple breakdown:

- ITR-1 (Sahaj): For salaried individuals with income up to ₹50 lakh, one house property, and interest income

- ITR-2: For individuals with capital gains, foreign income, or more than one house property

- ITR-3: For individuals with business or professional income

- ITR-4 (Sugam): For small businesses and professionals opting for presumptive taxation

Knowing what documents are needed for income tax filing and which form applies to you is the first step. Getting this wrong can lead to a defective return notice from the department.

When Should You Start Tax Planning - Beginning of Year or End?

This is where most people go wrong. They treat tax planning as a last-minute task. In reality, the best tax saving plan for salaried employees India starts on April 1st, not March 31st.

Here is why starting early makes a difference:

When you plan taxes in April, you spread your investments across 12 months. This means you invest in SIPs instead of lump sums. You get the benefit of rupee cost averaging. You have time to compare options under the old and new tax regime. And you are not forced into bad products just because the deadline is near.

Starting early also allows you to plan your advance tax payments properly. For salaried employees where TDS covers most liability, this may not seem urgent. But for business owners, freelancers, and professionals, advance tax must be paid in four installments - June 15, September 15, December 15, and March 15. Missing these leads to interest under Sections 234A, 234B, and 234C.

Moreover, many tax-saving instruments have lock-in periods. ELSS mutual funds have a 3-year lock-in. PPF has 15 years. Tax-saving FDs have 5 years. Investing in these without thinking about your liquidity needs is a mistake. When you plan early, you match your tax-saving choice with your financial goals.

So, when should you start? Today. Right now. The best time to plan your taxes for the current financial year is always the first day of that financial year.

Also Read - Business Loan Advisory Guide for Startups and SMEs in India (2026) – Complete Step-by-Step

How to Save Income Tax in India in 2026 - Top Deductions Explained

This is the section most people skip to directly. And that is fine. Here are the most powerful ways to reduce your tax liability under the income tax planning and filing in India framework.

Section 80C - Where to Invest to Save Tax

Section 80C is the most popular section in the entire Income Tax Act. Under this section, you can claim a deduction of up to ₹1.5 lakh per financial year by investing in approved instruments.

The eligible investments under income tax deductions under section 80C 80D include:

- PPF (Public Provident Fund) - safe, government-backed, 15-year tenure

- ELSS Mutual Funds - shortest lock-in of 3 years, potential for higher returns

- Employee Provident Fund (EPF) - automatic deduction from salary

- Tax-Saving Fixed Deposits - 5-year lock-in, guaranteed returns

- National Savings Certificate (NSC)

- Sukanya Samriddhi Yojana (for daughters below 10 years)

- Life Insurance Premiums

- Home Loan Principal Repayment

- Tuition fees for up to 2 children

The key is to choose instruments based on your risk appetite and liquidity needs, not just the tax benefit.

Did You Know? Section 80C has not been increased from ₹1.5 lakh since 2014. With inflation rising every year, tax experts and industry bodies have been repeatedly asking the government to raise this limit. However, as of 2026, it remains at ₹1.5 lakh - which makes every rupee invested under this section even more valuable.

Section 80D - Health Insurance and Tax Savings

Section 80D allows deductions on health insurance premiums. This is a section that almost everyone qualifies for, yet many people overlook it.

Here is the structure under income tax deductions under section 80C 80D:

- Up to ₹25,000 for health insurance for self, spouse, and children

- An additional ₹25,000 for parents below 60 years

- An additional ₹50,000 if parents are senior citizens (above 60 years)

So, if you are insuring yourself and your senior citizen parents, your total deduction under 80D alone can go up to ₹75,000. Add preventive health check-up expenses of up to ₹5,000 within this limit.

Beyond 80C and 80D, there are several other deductions worth exploring. Section 24(b) allows up to ₹2 lakh deduction on home loan interest. Section 80G covers charitable donations. Section 80E covers interest on education loans. Section 80TTA covers savings account interest up to ₹10,000.

Each of these can bring your taxable income down significantly - but only if you plan for them in advance.

Also Read - What is Bookkeeping and why every business need it? (2026 Guide)

Old Regime vs New Regime - Which Is Better for You?

This is the most debated question in personal finance today. And the honest answer is - it depends on your income and deductions.

Here is a simple way to think about it. Ask yourself one question: How much can you claim in total deductions?

The old regime vs new regime which is better question comes down to this comparison:

Under the Old Tax Regime, you pay higher tax rates but can claim all deductions - 80C, 80D, HRA, home loan interest, LTA, and more. If your total deductions exceed ₹3.75 lakh, the old regime usually wins.

Under the New Tax Regime, you pay lower tax rates but lose most deductions. Only the standard deduction of ₹75,000 is available for salaried employees. If you have very few investments or deductions, the new regime gives you a lower tax bill.

For most salaried employees earning below ₹10 lakh with active investments, the old regime still saves more. For young earners, those with fewer financial commitments, or those who prefer simplicity, the new regime is attractive.

The most important thing is to calculate both before deciding. Do not just assume. A tax advisor in Bhopal or your city can run this comparison for you in minutes using your actual income and deduction numbers.

Remember, the new tax regime is now the default option. If you want to switch to the old regime, you must explicitly opt for it while filing your return. Missing this step means you automatically fall under the new regime.

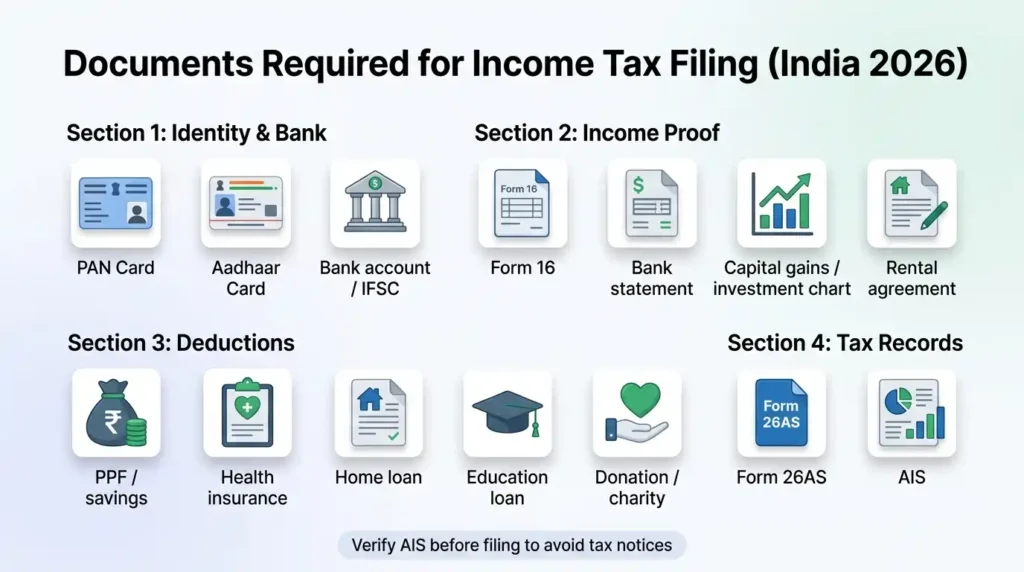

What Documents Are Needed for Income Tax Filing?

One of the biggest delays in filing returns comes from not having documents ready. Here is a complete list of what documents are needed for income tax filing:

Basic Identity & Bank Documents:

- PAN Card (mandatory)

- Aadhaar Card (must be linked to PAN)

- Bank account number and IFSC code for refund

Income Documents:

- Form 16 - issued by your employer, shows salary and TDS

- Form 16A - for TDS on bank interest, professional fees, rent

- Bank statements - to verify interest income

- Capital gain statements from brokers (for stock or mutual fund investments)

- Rental income proof - rent agreement and receipts

Deduction Proof Documents:

- Investment proofs - PPF passbook, ELSS statements, LIC receipts

- Health insurance premium receipts (80D)

- Home loan interest certificate (Section 24b)

- Education loan interest statement (80E)

- Donation receipts (80G)

Tax Credit Documents:

- Form 26AS - auto-generated tax credit statement from the IT department

- Annual Information Statement (AIS) - shows all financial transactions reported against your PAN

The AIS is especially important now. The Income Tax Department uses it to cross-verify your return. Any mismatch between your filing and AIS can trigger a notice. Always download and review your AIS before filing.

Also Read - Accounting and Bookkeeping Services in India: Complete Guide for Businesses

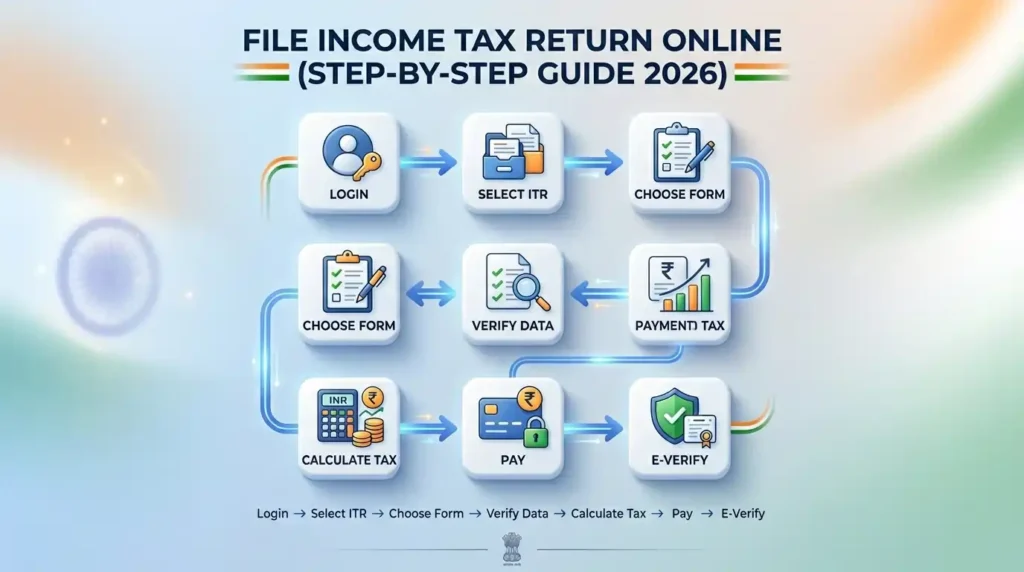

How to File Income Tax Return Online - Step-by-Step Process

Filing your ITR online is now straightforward. Here is how the process works for an income tax filing service on the government portal:

Step 1: Visit the Income Tax e-Filing portal at incometax.gov.in and log in using your PAN.

Step 2: Go to "File Income Tax Return" under the e-File menu. Select the correct Assessment Year - for income earned in FY 2025-26, select AY 2026-27.

Step 3: Choose your filing mode. Most individual taxpayers use online mode.

Step 4: Select the correct ITR form based on your income type (as explained earlier in this guide).

Step 5: The portal will pre-fill a lot of data from Form 26AS and AIS. Review each section carefully. Add any income or deductions that are missing.

Step 6: Verify your tax computation. If tax is payable, pay it online through the integrated payment module.

Step 7: Submit your return and complete e-verification using Aadhaar OTP, net banking, or Demat account.

Your return is not considered filed until e-verification is complete. Many people submit but forget to verify - their return then remains invalid.

If all of this feels confusing, that is completely normal. The process involves multiple forms, cross-verification of data, and knowledge of tax law. This is exactly why hiring a professional for your income tax filing service is a smart investment, not an expense.

Did You Know? Under the new Income Tax Act 2025, the deadline for filing revised returns has been extended to December 31 - giving taxpayers a full 12 months from the end of the Tax Year to correct mistakes in their original return. This is a significant taxpayer-friendly change from the earlier 9-month limit.

ITR Filing Last Date AY 2026-27 - Deadlines You Must Not Miss

Knowing the ITR filing last date AY 2026-27 is non-negotiable. Missing these dates leads to late filing fees, interest charges, and loss of carry-forward benefits.

Here are the key deadlines for AY 2026-27:

| Taxpayer Category | ITR Form | Deadline |

| Salaried individuals, pensioners | ITR-1, ITR-2 | July 31, 2026 |

| Business owners and freelancers (non-audit) | ITR-3, ITR-4 | August 31, 2026 |

| Businesses requiring tax audit | ITR-3, ITR-5 | October 31, 2026 |

| Companies with transfer pricing | ITR-6 | November 30, 2026 |

| Revised or belated returns | Any | December 31, 2026 |

Missing the July 31 deadline means paying a late filing fee of up to ₹5,000 under Section 234F. For taxpayers with income below ₹5 lakh, this fee is capped at ₹1,000.

Beyond the fee, missing the deadline also means you cannot carry forward capital losses or business losses to future years. This is a significant cost that most people underestimate.

Set a reminder today. File early. Do not wait for the last day.

Why Hiring a CA for Income Tax Planning Is the Smart Choice

Many people think filing taxes is a simple form-filling exercise. And for basic cases, it can be. But for most taxpayers - especially those with multiple income sources, investments, property, or business income - the decisions involved are far more complex.

Here is why working with the best CA for income tax planning makes sense:

They find deductions you miss. A good income tax consultant near me or in your city will often identify deductions you did not know existed. This alone can save more than their fee.

They keep you compliant. Tax laws change every year. A professional stays updated so you do not have to. This means no missed deadlines, no wrong forms, and no ignored notices.

They help you choose the right regime. Old regime vs new regime is not a simple calculation for most people. A CA runs actual numbers based on your income, deductions, and investments - not guesswork.

They handle notices. If you receive a tax notice, a CA knows exactly how to respond. Handling notices without professional help is one of the riskiest things a taxpayer can do.

They plan year-round, not just in March. The best tax advisor in Bhopal or your city will help you structure your income, investments, and business transactions across the full financial year - not just at the end.

The cost of a professional's fee is almost always lower than the tax you save with their help. And it is definitely lower than the penalties you avoid.

Also Read - Benefits of Hiring an Outsourced Accountant

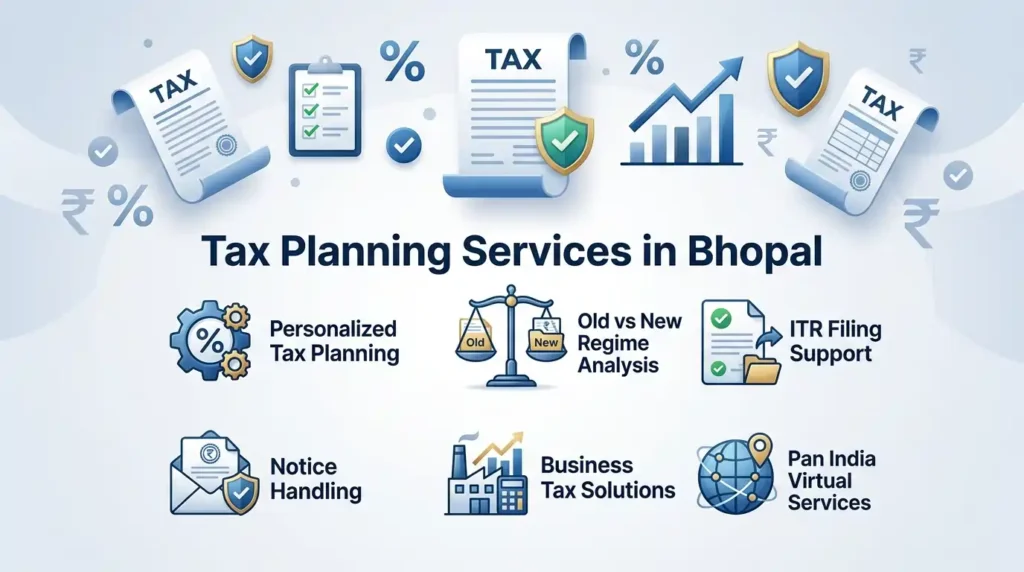

How CA Yash Garg Helps You With Tax Planning Service in Bhopal

CA Yash Garg is a practicing Chartered Accountant based in Bhopal, serving individuals, salaried employees, business owners, MSMEs, and corporate clients across India. With over 10 years of hands-on experience, the team has helped hundreds of clients reduce their tax liability, file accurate returns, and stay fully compliant with the law.

Here is what makes CA Yash Garg the preferred Income Tax Consultant in Bhopal:

Personalized Tax Planning: Every client gets a customized tax planning service based on their income, family situation, investments, and financial goals. There is no one-size-fits-all approach here.

Regime Selection Analysis: The team compares your tax liability under both the old and new tax regime using actual numbers - so you always pick the option that saves you the most money.

Complete Income Tax Filing Service: From collecting documents and verifying AIS/26AS to filing the return and completing e-verification, the entire income tax filing service is handled end to end.

Handling Notices & Scrutiny: If you receive a notice from the Income Tax Department, CA Yash Garg's team handles the response professionally, protecting your interests at every step.

Business Tax Planning: For business owners and self-employed professionals, the firm provides year-round tax management - including advance tax calculations, TDS compliance, and audit support.

Virtual Services: Clients across India can access all services remotely. You do not have to be in Bhopal to work with a trusted Tax Advisor in Bhopal who understands Indian tax law inside out.

Whether you are filing your very first return or managing complex business taxes, CA Yash Garg brings clarity, accuracy, and genuine care to every engagement.

Ready to Save More Tax This Year? Book Your Free Consultation Now

You have read the complete guide. Now it is time to act.

Every month you delay your income tax planning and filing in India is a month of potential tax savings going to waste. Whether you want to choose the right tax regime, maximize your deductions, or simply file your ITR without any stress - CAYashGarg is here to help.

Here is what you get when you connect with us:

- Free 30-minute tax consultation - no charges, no obligation

- Personalized tax regime comparison (old vs new) for your income

- Complete Income Tax Filing Service handled by qualified CAs

- Year-round Tax Planning Service tailored to your goals

- Expert support from a trusted Income Tax Consultant in Bhopal

Do not wait for March. Start today.

Call / WhatsApp: +91-735-492-8295 🌐 Website: cayashgarg.com 📍 Location: Bhopal, Madhya Pradesh | Serving clients Pan-India"In our firm, we go beyond numbers - we provide strategic financial guidance that empowers businesses and individuals to thrive." - CAYashGarg, Chartered Accountant, Bhopal