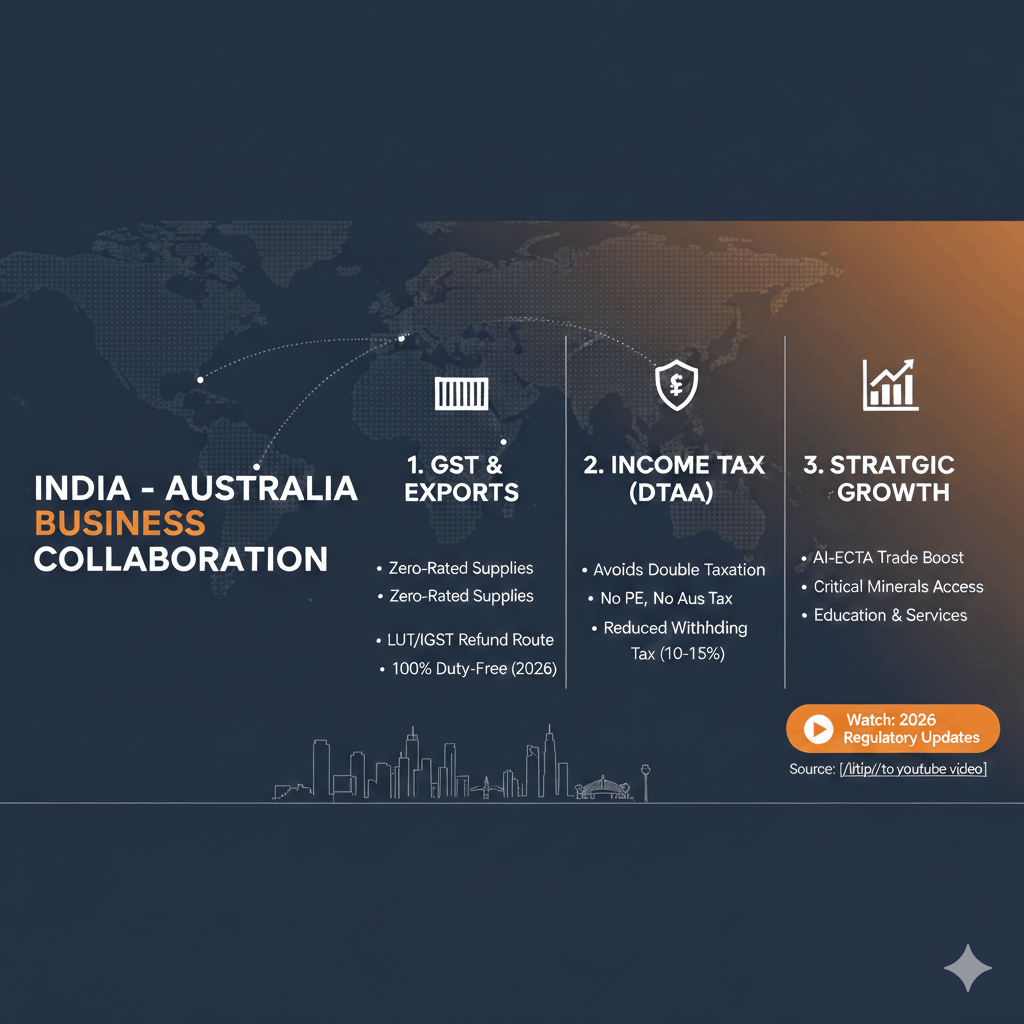

India – Australia Business Collaboration

GST, Income Tax and Strategic Benefits for Cross-Border Trade

India and Australia share a rapidly strengthening economic relationship, driven by policy alignment, trade liberalisation, and the Australia–India Economic Cooperation and Trade Agreement (AI-ECTA). For Indian businessmen engaging with Australian counterparts—whether through export of goods, provision of services, or joint ventures - the framework offers significant tax efficiency, regulatory clarity, and commercial opportunity.

This article outlines the GST implications, income-tax benefits, and broader business advantages of doing business between India and Australia.

1. GST Implications on India–Australia Business Transactions

Export of Goods under GST

Under the Integrated Goods and Services Tax Act, 2017, exports of goods from India to Australia qualify as zero-rated supplies (Section 16). This ensures that exports are effectively tax-free while preserving the credit chain.

Indian exporters may opt for:

- Export under Letter of Undertaking (LUT) without payment of IGST and claim refund of unutilised input tax credit; or

- Export on payment of IGST and subsequently claim refund of IGST paid.

This mechanism ensures no embedded GST cost on exports and enhances price competitiveness of Indian goods in the Australian market.

Export of Services

Supply of services by an Indian businessman to an Australian entity qualifies as export of services if the statutory conditions are met, including:

- Supplier located in India

- Recipient located outside India

- Place of supply outside India

- Consideration received in convertible foreign exchange

Such services are also zero-rated, enabling refund of input tax credits.

Common examples include IT services, consultancy, accounting, legal services, software development, and back-office operations.

Compliance Simplicity

In most cases, Indian exporters of goods or services are not required to obtain GST registration in Australia, keeping compliance limited to Indian GST laws and procedures.

2. Income-Tax Benefits under India–Australia DTAA

Avoidance of Double Taxation

India and Australia have entered into a Double Taxation Avoidance Agreement (DTAA), which ensures that income earned in cross-border transactions is not taxed twice.

The DTAA clearly allocates taxing rights between the two countries based on the nature of income and the presence of a Permanent Establishment (PE).

Taxation of Business Profits

Business profits of an Indian businessman are taxable only in India, unless the businessman has a Permanent Establishment in Australia, such as a branch, office, or fixed place of business.

In the absence of a PE:

- Australian income tax does not apply to business profits

- Indian tax laws govern taxation entirely

This offers clarity and certainty to Indian exporters and service providers.

Reduced Withholding Taxes

The DTAA provides concessional withholding tax rates on income such as:

- Royalties

- Fees for technical services

- Interest

By furnishing a Tax Residency Certificate (TRC) and filing Form 10F, Indian businesses can claim treaty benefits and reduce tax leakage.

Foreign Tax Credit

Where taxes are paid in Australia, Indian taxpayers are entitled to Foreign Tax Credit (FTC) in India under Section 90 of the Income-tax Act, ensuring relief from double taxation.

3. Trade Benefits under AI-ECTA

The Australia–India Economic Cooperation and Trade Agreement has significantly improved market access for Indian businesses.

Customs Duty Elimination

- More than 96% of Indian exports to Australia are duty-free

- Key beneficiary sectors include textiles, engineering goods, pharmaceuticals, leather products, jewellery, and chemicals

This has substantially enhanced the competitiveness of Indian exports in the Australian market.

Improved Trade Facilitation

The agreement promotes:

- Faster customs clearance

- Reduced tariff and non-tariff barriers

- A predictable and transparent trade environment

These measures reduce transaction costs and encourage long-term commercial relationships.

4. Broader Commercial and Strategic Advantages

Stable and Transparent Business Environment

Australia offers a robust legal system, strong contract enforcement, and regulatory stability, making it a low-risk destination for Indian businesses.

Access to a High-Value Market

Australia’s high purchasing power and demand for quality products and professional services enable Indian businesses to move from volume-driven trade to value-driven exports.

Ease of Doing Business

Key factors facilitating ease of operations include:

- English-speaking market

- Comparable accounting and compliance standards

- Efficient banking and remittance systems

Emerging Opportunities

Significant opportunities exist in:

- Information technology and digital services

- Education and skill development

- Healthcare and pharmaceuticals

- Mining support services

- Joint ventures and start-up collaborations

Conclusion

Business engagement between Indian and Australian businessmen presents a strategically sound and tax-efficient opportunity. With zero-rated GST exports, income-tax certainty under DTAA, and trade liberalisation through AI-ECTA, the India–Australia corridor offers a compelling platform for global expansion.

For Indian entrepreneurs and exporters, Australia is not merely a destination market—it is a long-term strategic partner.